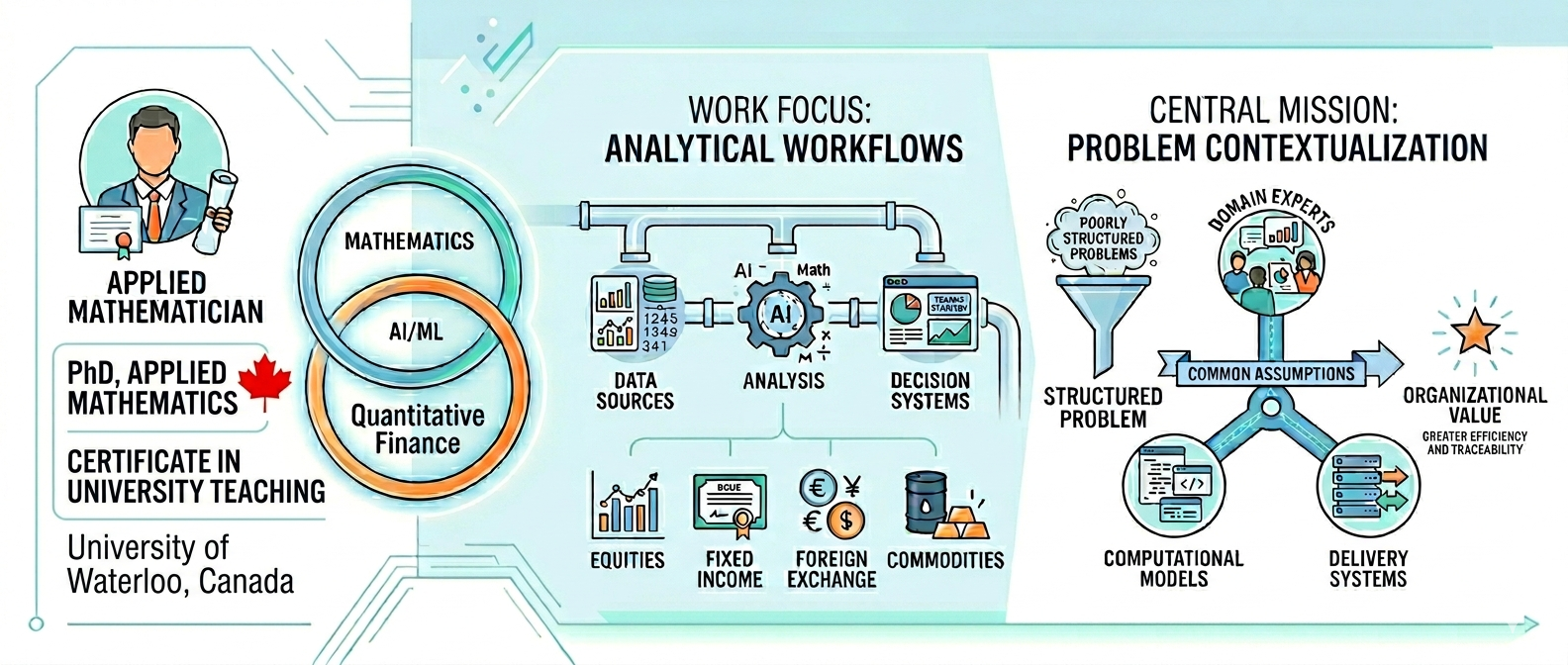

Bio

My academic research centers on developing analytical models to understand and predict complex systems, with particular emphasis on Inverse Problems (Hyper-Parameter Optimization), non-smooth optimization, network analysis, and computational science. My previous work examined co-expression networks and the behavior of intracellular networks in type 2 diabetes and cancer cells. For details see my Research Page

My industry work focuses on developing trading & investment signals, risk models, and quantitative portfolio management across asset classes including equities, fixed income, foreign exchange (FX), and commodities. A central theme of this work is the translation of business problems into structured analytical frameworks that generate long-term value for the organization. This process incorporates domain expertise, enabling data, models, and analytical infrastructure to operate from a shared set of assumptions while being adapted into AI-agentic workflows. In practice, this approach produces reusable agent artifacts analogous to Visual Studio Code Agent Plugins, with the broader objective of generating organizational value more efficiently. For additional details, see the Professional section.

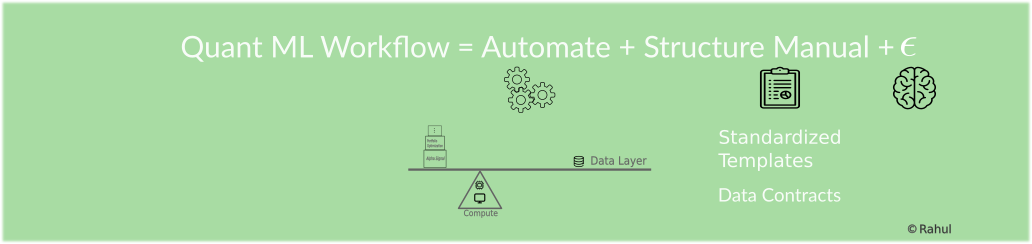

Example Method

\[ \mathrm{Contextual\ Engineering\ Workflow} = \text{Automation} + \text{Structured Manual Knowledge} + \epsilon \]

In this formulation, \(\epsilon\) denotes the irreducible domain uncertainty that still requires expert interpretation. Figure Figure 2 summarizes the method schematically and highlights why resilient analytical processes must accommodate exceptional events, including systemic disruptions such as the COVID-19 pandemic.

Professional

I currently work at Commerzbank AG, Frankfurt, Germany as a Data Scientist with a forward development engineering mandate within the AI team in Sales Analytics. My work is organized around two related objectives:

- Identifying information anomalies in market data for trading-signal development

- Translating current trading processes, together with both legacy and newly developed models, into AI-agent-based workflows.

Currently, working with the commodities and FX desks, I focus on building analytical processes into reusable agent-based systems and on connecting trading-signal generation to in-house quantitative infrastructure. The role combines:

- Business-logic formalization with the translation of expert judgment into reusable context for AI agents.

- It also involves integrating AI agent outputs into trading practices and aligning to institutional constraints to improve analytical efficiency and support higher-value decision-making.

Previous Experience

My previous industry experience spans asset management, systematic equity investing, and commodity trading. At Finance in Motion, I worked as a quantitative analyst, where I developed risk-adjusted asset-allocation approaches for bond portfolios and built an internal credit-risk model based on the CreditMetrics methodology. At PineBridge Investments, I worked in systematic equity strategy, focusing on portfolio management, investment-platform development, and factor-based investment-signal generation using machine learning. At Trafigura, I worked with the liquefied natural gas (LNG) desk, developing hedging strategies and proprietary methods for identifying cointegrated time series. At BlackRock, I worked in systematic equity strategy with a focus on machine-learning-based factor signal generation and investment-platform development.

My earlier academic work spans systems and computational biology, electronic sciences, and applied environmental modeling. This portfolio includes research on conducting polymers for solar energy harvesting, as well as meteorological analysis conducted in collaboration with the Indian Meteorological Department, where I developed a regression framework to examine how temperature and pressure influence humidity-sensor response.